Polaris Infrastructure – Large Discount to NAV, Attractive Return Potential

Summary

High IRR (30% – 50%) investment opportunity with near term catalysts.

Fixed balance sheet and new management provide attractive risk / return profile.

Should be near-term dividend payer.

Editor’s Note: Polaris Infrastructure trades with much greater liquidity on the TSX under ticker PIF.

Company: Polaris Infrastructure (Formerly Ram Power) (RAMPD)

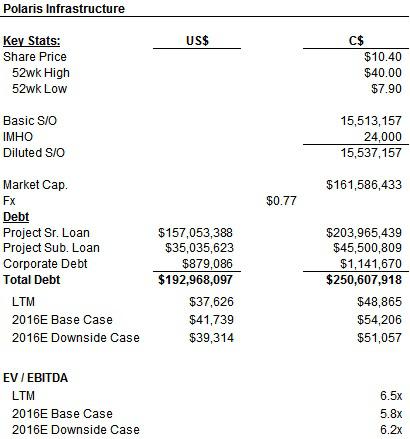

Market Cap: C$160MM

Debt / Leverage: US$193MM (Almost all project level debt) 5.0x Debt / EBITDA, 3.2x Net Debt / EBITDA

Key Metrics: ~6.5x EV / EBITDA

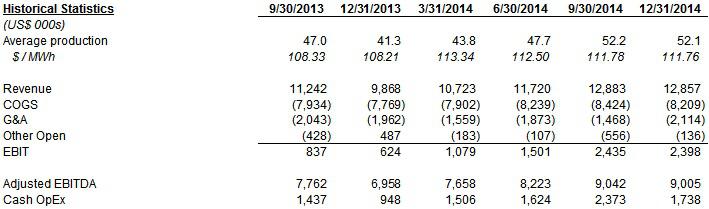

Description: Polaris Infrastructure is a Canadian Listed, thermal energy company with a producing asset in Nicaragua. Their producing asset (San Jacinto-Tizate) had faced substantial operational issues, falling short of expected production, which ultimately led the company to a substantial equity re-capitalization led by Goodwood in 2015. The company was formerly RAM Power, with an improved balance sheet, new management and 8 quarters of materially stable energy production the risk reward to equity investors is attractive. A prior credit facility significantly constrained the Company’s ability to provide dividends due to operational covenants but revised terms provide operational and financial breathing room.

Management: There has been interim executive team in place since 2013 through to the re-capitalization. New management has a focus on transitioning from being a developer to managing a sustainable, stable, incremental growth business.

Shareholders: Relatively widely-held: Goodwood (11.5%), Sentry (7.3%), PenderFund (3.7%)

Investment Thesis:

1) Switch to substantial equity FCF generation as new credit terms will allow for cash to flow out of operating company to shareholders with potential dividends (est. 2016 catalyst)

2) PPA’s in place provide stable revenue, Contract $/MW rate are at a discount to spot market

3) No analyst coverage, limited investor awareness

4) M&A, stable infrastructure asset should appeal to international peers given cleaned-up/simplified balance sheet, significant trading discount

Valuation and Return Analysis:

Polaris trades at a substantial discount to some the small-cap infrastructure peers (~6.0x EV/EBITDA vs. ~12x average for Canadian IPP and Alternative Energy peers (8.0x – 16.0x Range as per Industry research)

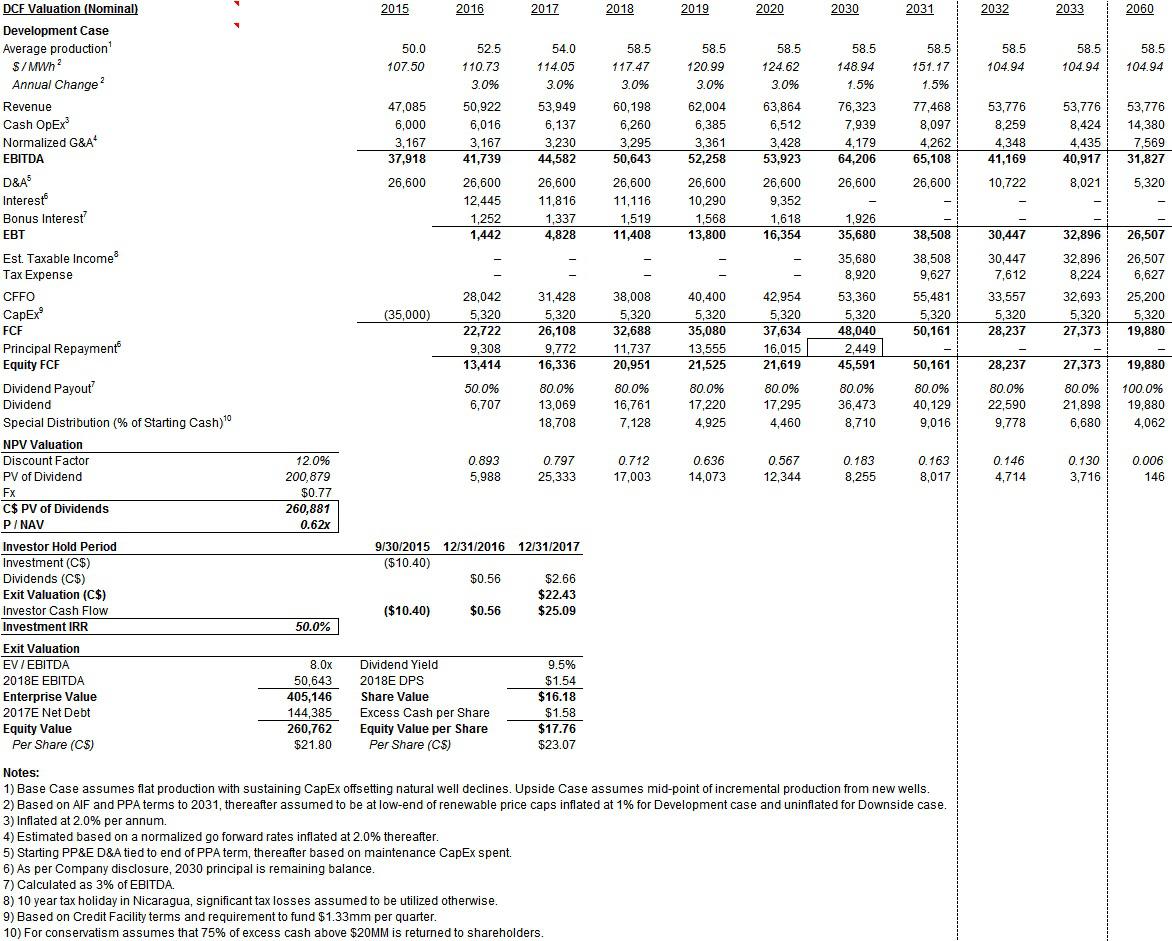

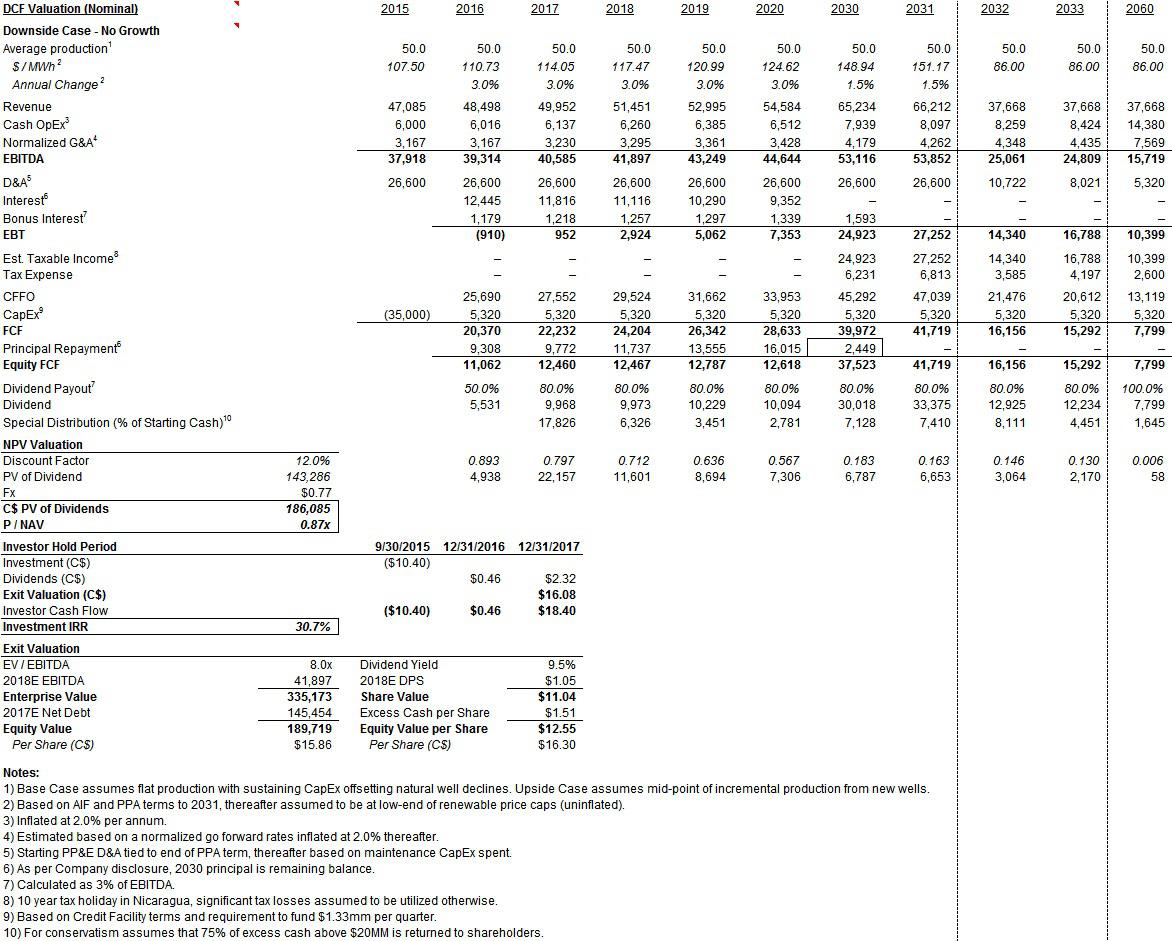

Currently the Company trades at 0.62x P/NAV based on an equity level DCF valuation done at a 12% discount rate, the Development Case assumes three wells are drilled and lead to 8.5MW of incremental growth (a discount to the current production of ~50MW from 8 producing wells) and contracted prices to 2031 and conservative pricing from 2032 to 2060. For the downside case we assumes that the $35MM of capital is drilled but it fails to produce any incremental MW and that pricing after 2032 is in a worst case rate. the Company trades at 0.87x P/NAV at a 12% discount rate.

Over a 27 month holder period investors would see 30% – 50% IRR assuming the Company begins paying stable dividends and trades closer to peers (8.0x EV / EBITDA and 9.5% Yield).

Other Considerations / Risks:

PIF operating income is based on US$ with valuation back to a C$ through its TSX listing.

While there is a PPA in place through 2032, there is some execution risk thereafter where a new PPA may be priced in below current agreed rates (as modeled in both scenarios). The facility and the geothermal power is exposed to reservoir risk and is dependent on future drilling of wells to facilitate the production of steam. As such there is arguably less operational certainty and/or more potential on-going capex then solar / wind or other renewables. The company is focusing on a near-term drilling capex program (~$35mm) which may not be successful. Cash flows to equity is dependent on meeting certain covenants.

The Companies exploitation agreement requires that it reach 90% of name plate production which it has failed to meet, to date the company has been able to rely on a force majeure characterization, and has until May 2016 to resolve the issues. Speaking with management the requirement falls away with an incremental $25MM in CapEx being spent by May, which is captured in their $35MM CapEx program, and meeting a new lowered production of ~46MW.

Investing in operation in Nicaragua poses geo-political risk.

Upside:

M&A potential as company trades at a discount to peers. Company may seek to monetize undeveloped assets, potentially through a JV. Other projects: Bottoming Unit ($25mm CapEx, 6-7MW) provides incremental upside which the Company may be able to fund through a low cost international development bank. In addition the Company has another project Casita which is believed to be feasible but no value has been attributed in this analysis.

Disclosure: I am/we are long PIF ON THE TSX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The analysis presented is for illustrative purposes only.